excerpt

http://seekingalpha.com/instablog/234091-hewitt-heiserman/61457-rare-cardinal-climax-planetary-alignment-this-summer-puts-stocks-at-risk-says-veteran-sky-watcher

Rare “Cardinal Climax” Planetary Alignment This Summer Puts Stocks at Risk, says Veteran Sky Watcher

This summer the planets form a rare “Cardinal Climax” alignment, which puts financial markets at risk, says Arch Crawford. Publisher of Crawford Perspectives since 1977, the veteran sky watcher uses a mix of technical analysis and astrology to gauge which way equities and other asset classes are headed. To learn more about this unorthodox investment process, I recently spoke to Mr. Crawford about some of his best calls, what day the Cardinal Climax strikes, and how to prepare for the turmoil he expects. Here is an edited version of our conversation.

We want to talk about the upcoming Cardinal Climax, which you say puts stocks—and perhaps humanity—in jeopardy. But first, explain to Seeking Alpha readers how you invest?

Certain planetary alignments put people under extra stress. And one way this stress manifests itself is in financial markets. After all, financial markets are a mix of fundamentals and emotion. Since astrologic events affect our emotions, I find it profitable to study the planets.

Tell me more.

It is common knowledge that when there is a full moon, there are more car accidents and other forms of aggressive behavior. Since financial markets partly reflect our hopes and fears, these markets are prone to mood swings. If you can anticipate these mood swings, you gain an edge over investors who focus solely on interest rates, growth forecasts, debt loads, and other traditional yardsticks.

I have examined every substantial move in the Dow Jones Industrial Average since 1896, and I find that when planets are at difficult angles, then owning stocks and commodities is riskier.

What is a “difficult” angle?

When two planets form a 45-, 90-, 135-, or 180-degree angle, with earth as the midpoint between the two planets.

Why do difficult angles cause difficult markets?

The reasons are partially understood. In the 1940’s, radio propagation specialist John Nelson studied planetary alignments to time sunspot activity and solar flares, and thereby help his employer, RCA, reroute shortwave radio transmissions efficiently. Years later, when I got interested in alignments and became friendly with John, he would tell me when a flare was in progress. I would then call a broker and find that, typically, stocks were dropping and gold was rising. In concert with new and full moons, where the tidal forces brought the atmospheric disturbances closer to the earth, extreme volatility would ensue in markets where a significant emotional component was already in progress.

For instance, the highest sustained period of ionospheric electrons measured by geosynchronous satellite took place the week before and during the October 1987 crash, and then dropped back on the day of the stock market low.

Recent studies by physicists, biologists and cosmologists show gravitational and electromagnetic activity affects the growth patterns of many species here on earth. Much of this data was collected and correlated by the Foundation for the Study of Cycles, in Albuquerque, NM.

I once did a study of the worst days in the stock market. Two-thirds of those days occurred in one-third of the calendar year, centered on the Fall Equinox, around Sept. 22-23. Maybe there is a symmetry that governs the universe that we haven’t yet figured out.

How did a physics and math major from the University of North Carolina get interested in planets?

I read about it on the front page of the Wall Street Journal in 1963, while a technical market analyst at Merrill Lynch. I was the first assistant to the legendary Robert Farrell, who was repeatedly voted best on the Street by his peers in the annual Institutional Investormagazine poll. My curiosity piqued, I looked into this subject and found that difficult alignments correlated with difficult markets. The correlation was too well-defined to be chance.

Give us examples when difficult alignments correlated with difficult markets. Let’s start with the Great Depression.

During 1929-1932 there were several difficult planetary alignments.

What about the October 1987 crash?

On Aug. 24, planets were in the tightest five-body “conjunction,” or same ecliptic longitude, in at least 800 years. “It doesn't get any better than this,” I reasoned. Therefore, “A severe decline will follow,” I told subscribers. Turns out, Aug. 24 was the top. From that alignment high to the Oct. 20 low, the Dow fell 33%. A difficult planetary alignment preceded a difficult stock market.

What about the 2008 Crash?

Our research showed a Mars-Uranus “crash cycle” beginning Aug. 6, 2008 and ending in late-Mar. 2009. So beginning several months before Aug. 6, we repeatedly told subscribers, “Neither Wall Street nor our Government will be able to hold markets up against the 'deluge'!"

Further, on Sept. 2 we told subscribers that the worst part of the crash would occur on Oct. 10, plus or minus three trading days. We repeated this forecast on Oct. 2. Our headline was: “Market Crash – Dead Ahead.” Turns out, Oct. 10 had the largest number of new lows on the NYSE ever, at 1203.

Why did you choose Oct. 10?

There was a full moon after the market closed on Oct. 9. Also, there was a “Grand Cross” alignment at this time, with the sun opposite the moon, and squaring Uranus opposite Neptune.

So this is another example of when a difficult planetary alignment preceded a difficult stock market.

Did the planets or your technical analysis forecast the rebound in stocks which began March 9, 2009?

Our March 2 headline was: "Best Bet - Nearby Low!"

Then on March 12 we told subscribers: "We believe this rally confirms a strong buy.”

Does energy from difficult alignments reveal itself in ways that go beyond financial markets?

In April 1986 we had a Lunar Eclipse conjunct Pluto. The close proximity with Pluto is rare. So we told subscribers, "If you don't feel this one, you're not alive!" We were prophetic, as the April 26th Chernobyl accident raised radiation levels worldwide.

By the way, we have another Lunar Eclipse conjunct with Plato on June 26. Pluto “rules” nuclear power, debt, interest rates, and the use of force, say the astrologers. Maybe June 26 is the de facto start of the Cardinal Climax.

In November 1989, we observed a Saturn conjunct with Neptune, both opposite Jupiter to the day. This alignment happens every hundreds of years; i.e., it is extremely rare. Several days later the Berlin Wall fell.

In our July 1990 we told subscribers, “This will be one of the worst days of the century. There will be coercion, the use of force, a large explosion and heartlessness or cruelty August 2-7." On Aug. 2, Saddam Hussein unexpectedly attacked Kuwait. What alarmed me was the Lunar Eclipse forming another Grand Cross, this time with Mars opposite Pluto.

What about September 11, 2001?

In our letter mailed Sept. 4 we wrote that when Mars hits the solar eclipse point on Sep. 7th or Sep. 8th, then the U.S. will be at war.

Do the planets ever fool you?

We are still in the 'covered wagon days' of this as a science. Much of the time is without major significance. Also, the “big alignments” can be tricky to interpret. But some alignments—this summer’s Cardinal Climax, for instance—are unambiguous.

Let’s talk about the Cardinal Climax.

On August 1, give or take a week, we’ll have the most five-planet alignments in perhaps thousands of years. Known as the “Cardinal Climax,” this is the meanest, nastiest, most challenging and most transformational of any planetary phenomena in all of written history!

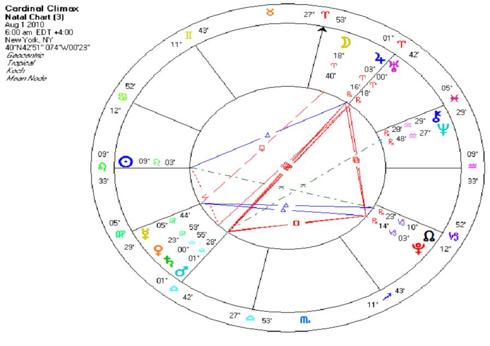

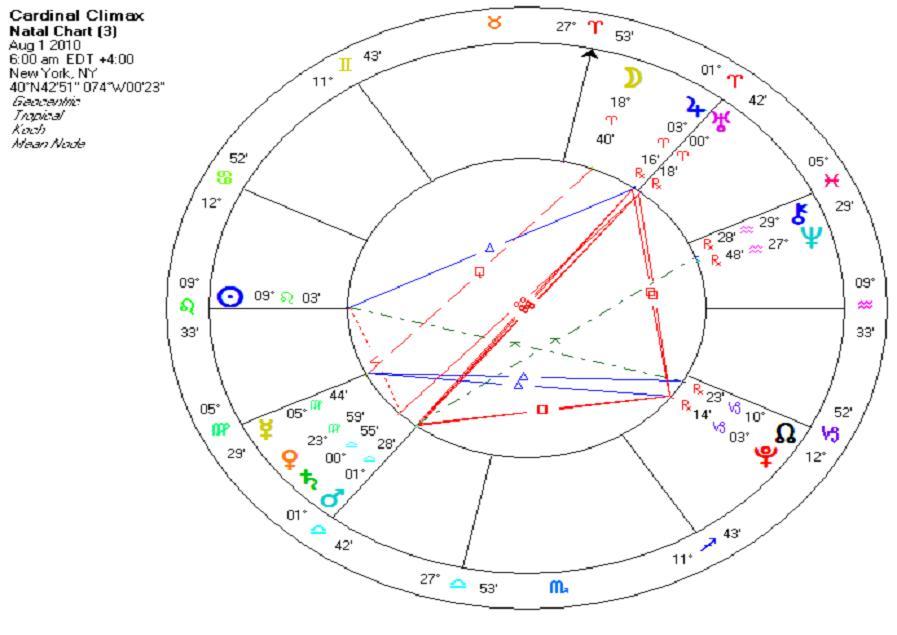

We’re giving readers a link to a chart showing the Cardinal Climax.  What do you see?

What do you see?

What do you see?

What do you see? This is the view of the planets from New York City on Aug. 1, at 6am. We have the most planets in the tightest alignments and at the supposedly 'sensitive' Zero degrees of Cardinal signs. It makes the hair on the back of my neck stand up.

I looked at records going back to the 1800’s, and this is the most difficult alignment I found. When I was at a conference in Boston last month, someone said this was the most difficult alignment they have seen in the last "1,000 years." Another person told me this is the worst alignment in "10,000 years."

What are possible consequences?

Worst cases include a nuclear accident. Nuclear war. Massive societal collapse. Maybe a pole flip, which can wipe out nearly everything.

Cardinal Climax is especially intimidating because of the proximity to the widely touted Mayan Calendar End Date. Plus, the Christians are looking for the Return of Jesus and/or the Rapture, the Muslims await the return of the umteenth Imam, the White Buffalo has been born, and Jews are fighting over the right to rebuild Solomon's Temple on the 'temple mount' in Jerusalem. These are all signs of “end times” by many different cultures.

The one thing most convincing to me is that there are more people alive on the planet today than all who have ever lived in recorded history. So it may be that every soul is on board for this event!

At a recent 1180, did the S&P 500 already peak for 2010?

The top may be this month or in May, based on normal seasonal and astrologic patterns.

Will Cardinal Climax cause just U.S. stocks to fall? Or is this a global meltdown?

Definitely global.

If I sell my stocks, as you advise, where do I put my money?

The best money will be made on the downside in shorts, stock index futures, negative ETF’s, and put options. However, we do not recommend that subscribers buy options—especially if they are not seasoned traders. With options, you can get the direction right but then maybe not get paid in usable currency before the whole system melts down.

Inflationists advise buying commodities, to protect against the 21% year-over-year increase in Federal Reserve assets, and the 15% year-over-year increase in U.S. public debt.

We are probably seeing a peak in general optimism about the economy and commodity prices. When suspicion arises that a double dip or worse is about to return, we will see the commodity averages slip into the tank. Even assets in the ground will not hold against a worldwide depression that is well on its way.

Deflationists say buy long-term U.S. Treasuries, because it will take years to reduce a 375% debt-GDP ratio, and because the M1 money multiplier is barely pulsing, at 0.8x.

We’d rather be long German, Swiss or Australian bonds, although U.S. bonds will probably do well on the initial declines. Do not overstay as the U.S. Dollar will come down hard. The United States will come apart in this Depression!

Besides selling stocks, what other precautions do you advise?

Our markets may be the least of our worries, given this powerful and chaotic frame. The Mormon mandate of keeping two years worth of food and water in your home is common sense.

How do we know when it is safe to own stocks again?

"When CNBC becomes a sports station!,” to quote my friend Jim Grant.

You have 55 years of investing experience. What have you learned?

Nearly all of our frustrations in the market result from our unfulfilled expectations about what we thought a market ‘should’ do. No one knows the future.

Also, investing is probabilistic. So if you think knowing how to ‘read’ planetary alignments increases your probability of success, then get planetary literate.

Thank you, Mr. Crawford.